Examine This Report about Mortgage Investment Corporation

Examine This Report about Mortgage Investment Corporation

Blog Article

The 10-Second Trick For Mortgage Investment Corporation

Table of Contents3 Simple Techniques For Mortgage Investment CorporationAn Unbiased View of Mortgage Investment CorporationThe 6-Minute Rule for Mortgage Investment Corporation

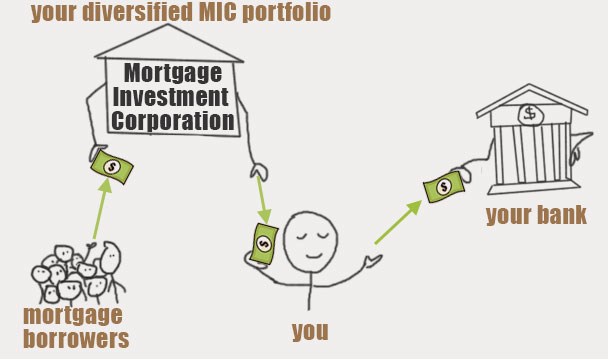

This suggests that investors can enjoy a steady stream of capital without needing to proactively manage their financial investment portfolio or bother with market changes. Additionally, as long as customers pay their home mortgage promptly, earnings from MIC investments will certainly stay stable. At the exact same time, when a borrower stops paying on time, capitalists can count on the knowledgeable team at the MIC to handle that situation and see the lending through the leave process, whatever that looks like.

As necessary, the purpose is for investors to be able to gain access to stable, long-lasting capital generated by a huge funding base. Returns obtained by investors of a MIC are normally classified as rate of interest revenue for objectives of the ITA. Resources gains realized by a capitalist on the shares of a MIC are typically subject to the normal treatment of resources gains under the ITA (i.e., in most scenarios, exhausted at one-half the rate of tax on average revenue).

While particular requirements are relaxed until soon after completion of the MIC's initial monetary year-end, the adhering to standards have to generally be pleased for a firm to get approved for and keep its standing as, a MIC: homeowner in Canada for objectives of the ITA and included under the laws of Canada or a province (special regulations put on firms included before June 18, 1971); only undertaking is investing of funds of the firm and it does not take care of or establish any type of real or immovable residential or commercial property; none of the residential or commercial property of the corporation includes financial debts having to the corporation secured on real or unmovable residential property found outside Canada, debts possessing to the company by non-resident persons, except financial debts safeguarded on genuine or immovable building positioned in Canada, shares of the funding stock of corporations not homeowner in Canada, or genuine or immovable building positioned outdoors Canada, or any type of leasehold interest in such residential or commercial property; there are 20 or more investors of the company and no investor of the straight from the source company (with each other with specific individuals associated to the investor) owns, straight or indirectly, more than 25% of the provided shares of any course of the capital stock of the MIC (particular "look-through" guidelines use in respect of trust funds and partnerships); owners of preferred shares have a right, after repayment of recommended dividends and repayment of rewards in a like amount per share to the owners of the usual shares, to participant pari passu with the owners of usual shares in any additional reward payments; at the very least 50% of the price amount of all residential property of the corporation is bought: financial obligations safeguarded by mortgages, hypotecs or in any type of various other manner on "homes" (as defined in the National Real Estate Act) or on property included within a "housing job" (as specified in the National Real Estate Act as it continued reading June 16, 1999); down payments in the documents of the majority of Canadian banks or cooperative credit union; and money; the expense amount to the company of all actual or unmovable property, including leasehold interests in such home (leaving out particular quantities acquired by repossession or according to a borrower default) does not go beyond 25% of the price quantity of all its property; and it follows the liability thresholds under the ITA.

The Mortgage Investment Corporation Diaries

Resources Structure Private MICs normally released two classes of shares, common and preferred. Common shares are generally issued to MIC owners, supervisors and policemans. Typical Shares have voting rights, are typically not qualified to rewards and have no redemption function but take part in the distribution of MIC properties after liked shareholders receive built up however unpaid dividends.

Preferred shares do not commonly have ballot legal rights, are redeemable at the option of the owner, and in some instances, by the MIC. On winding up or liquidation of the MIC, favored investors are usually entitled to obtain the redemption value of each preferred share along with any type of declared yet unsettled dividends.

One of the most frequently relied upon syllabus exceptions for personal MICs distributing securities are the "recognized investor" exception (the ""), the "offering memorandum" exemption (the "") and to a minimal extent, the "family members, close friends and service associates" exemption (the "") (Mortgage Investment Corporation). Capitalists under the AI Exemption are typically greater net worth capitalists than those who might only satisfy the limit to invest under the OM Exception (depending on the territory in Canada) and are most likely important site to invest greater quantities of funding

An Unbiased View of Mortgage Investment Corporation

Capitalists under the OM Exemption generally have a reduced total assets than certified capitalists and depending see here now upon the territory in Canada are subject to caps appreciating the quantity of funding they can invest. In Ontario under the OM Exception an "qualified capitalist" is able to spend up to $30,000, or $100,000 if such financier gets suitability recommendations from a registrant, whereas a "non-eligible financier" can only invest up to $10,000.

These structures assure consistent returns at much greater returns than conventional fixed revenue financial investments nowadays. Dustin Van Der Hout and James Price of Richardson GMP in Toronto assume so.

Report this page